Data Room Expectations

This week we cover what to include in a data room, how investors think about market size, and why a term sheet begets more term sheets.

Greetings! We hope you’re having a great week.

🚪Investor Data Room Expectations

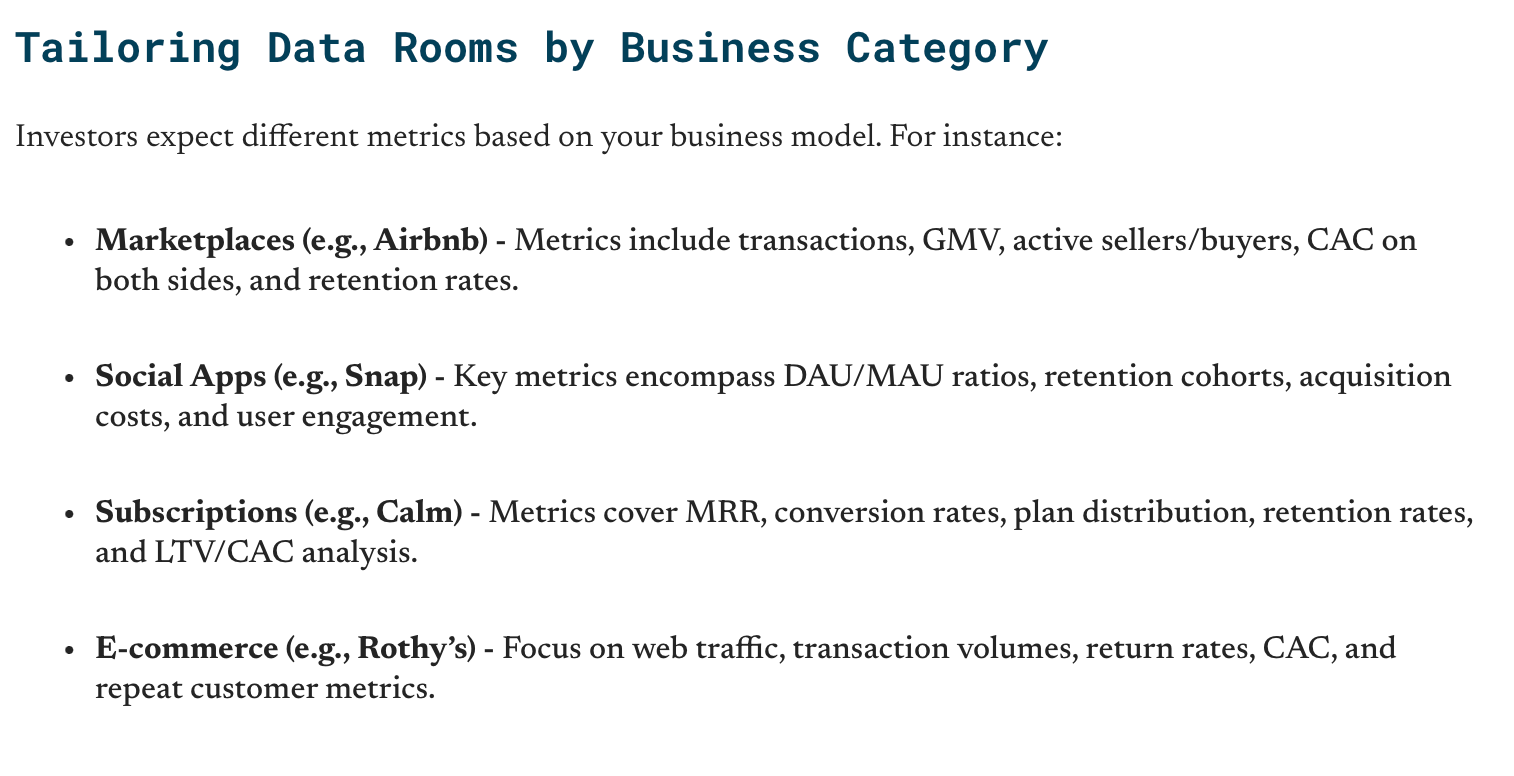

The data room is a critical part of any venture capital fundraise, but the contents of one and what investors expect to see can seem a bit ambiguous. GoingVC’s latest article sheds light on this by providing data room best practices and a checklist of important items founders should include in it. GoingVC outlines a pitch deck, cap table, historical P&L & burn, and usage data as the essentials.

STV Take: The above image highlights specific metrics investors might care about depending on the type of business being built. There is not necessarily a “right way” to build a data room; investors will have slightly different things they look for depending on stage and type of business, which I think is why there is some mystery around what exactly to include.

While it can take time to create a well put together data room, it is worth the effort. A good data room builds a founder’s credibility with investors and can streamline the diligence process for both founders and investors. If the data room is organized and robust without being overwhelming, it reduces the number of questions a founder has to field about where or what a document is, freeing up everyone to focus on the questions that materially matter for investors.

🗺️ A Guide to Optimizing Financial Performance

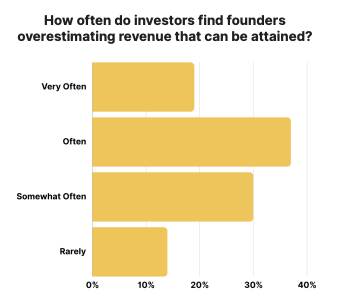

AVL Growth Partners released a new guide that highlights the key three financial drivers of a startup, along with recommendations on how to project business growth and avoid common financial modeling pitfalls. A few of the common mistakes AVL Growth discusses in this guide include:

Overestimating attainable revenue

Misunderstanding how quickly revenue can grow related to COGs

Underestimating customer acquisition cost

STV Take: Investors understand that a company’s revenue expectations and growth projections presented in a pro forma are educated guesses at best and shots in the dark at worst. Investors can sniff out the latter. While uncertainty is inevitable regarding early revenue growth, there are techniques and best practices founders can use to generate a solid understanding of their cost drivers and present realistic expectations for potential revenue growth. AVL Growth’s latest guide offers valuable tips to help founders craft the best version of their pro forma. (Sponsored)

🦄 Everything Changes with a Term Sheet

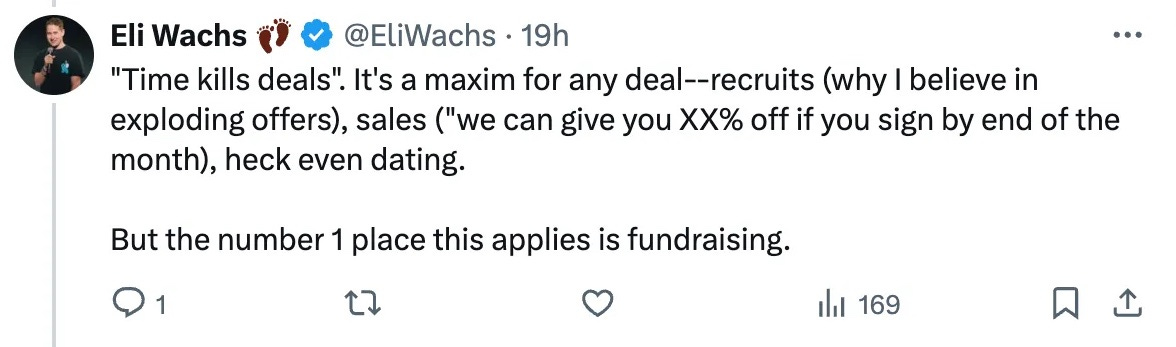

Eli Wachs presents an X thread that discusses how receiving a term sheet changes the dynamics of a round. It covers some of the psychology and firm dynamics that can cause VCs to come back around after a term sheet has been issued, while providing practical advice for founders on how to secure that first term sheet.

STV Take: I am skeptical of many X threads, but this one is an exception to a lot of the noise. Getting an investor to believe in the business and write the first term sheet is the hardest part of fundraising, but once it has been secured, the optics around the business change. Suddenly, it has validation and has been derisked to a certain degree. While a term sheet can be useful to getting investors to commit, it isn’t the only way. As Eli mentions, having great metrics is the ultimate way to instill confidence in the business. This is a good reminder that despite all of the psychology around successfully fundraising, the best unlock for securing investment is to be building a great business. Admittedly, that can be hard to demonstrate at the earliest stages, which is why any amount of derisking that can be done is beneficial to securing investment.

🏛️ Market Size & Opportunity Due Diligence

Seraf interviewed angel investor, Chris Mirabile, on how he approaches market due diligence for any potential investment. The discussion focuses on Chris’s perspective on the characteristics of investable markets, such as those with high fragmentation or one where a technical innovation is needed but only a third-party can deliver a truly independent, valuable product. Chris also discusses market size and why it’s so important for potential investors.

“The key to growing a company is finding a big enough market of willing buyers who can be accessed in an affordable way (relative to their lifetime value). The product may be good, and there may be lots of people who might buy it, but unfortunately a company’s true market is limited to those customers for whom that purchase addresses a top pain point and a top buying priority.”

— Chris Mirabile

STV Take: Chris does a good job of breaking down the math behind why market size matters so much to investors. The one place where I, along with probably most institutional investors, disagree with him is on the minimum market size investors want to see. He mentions $100M as the bare minimum, but I’d argue it’s closer to $1B. One of the examples he talks through is a startup operating in a $100M market. Even in the best of circumstances, it’s hard for investors to net a 4.6X return, which is a good but not ideal outcome, given the high failure rate in an investor’s portfolio. As cliche as it sounds and as frustrating as it can be for founders to hear that a market isn’t big enough, the underlying math makes it clearer why market size is so important.