Harsh Fundraising Truths

This week we bring some tough love about raising VC, Seed data from NYC-based companies, and thoughts on finding a buyer for a startup.

Greetings! We hope you’re having a great week!

💔 Fundraising Advice: The Tough Love Edition

Steph Nass from OpenVC took to X to explain why his fundraising guidance isn’t always the most optimistic, and in fact, quite contrary to the advice the tech ecosystem preaches. Steph explains that the chances of receiving venture funding for a business is quite low and most of the fundraising advice out there is a disservice to founders because it is designed for those with a track record. While dreaming big is a prerequisite for raising venture capital, Steph believes that the seemingly harsher, more conservative advice is sometimes what founders need to hear.

STV Take: While I believe everyone should have access to the means to achieve their dreams, raising venture capital doesn’t have to be the only path. The truth is most founders won’t be able to raise venture capital for a variety of reasons. It could be because the business they’re building isn’t a fit for venture capital or the team needs to demonstrate their entrepreneurial chops before investors can get comfortable. Whatever the case, pursuing venture capital can be time consuming and may divert attention from other valuable opportunities.

Steph’s post, while somewhat abrasive, offers a necessary reality check for those at the earliest stages of building. It highlights just how challenging it can be to raise funds, especially for those who are still “unknown quantities” and building their reputation. If you’re curious what a “known quantity” is or how Steph thinks about the top 10% of founders, he includes a chart in the response section.

🛬 Landing the Plane

On X, Frank Rotman, Co-founder and Partner at QED Investors, discusses the rarity of an IPO outcome for a startup and how founders and investors should respond once it’s clear that a company will not achieve the “escape velocity” needed to IPO. Frank notes that “landing the plane”—in other words, finding a strategic buyer that can allow the product and mission to continue—requires a lot of forethought and finesse. In the post, he outlines three high-level steps—1. Agree to land the plane, 2. Prepare for a sale, and 3. Run an organized M&A process—and provides insights and advice on each.

“How many Founders does it take to land a plane? None, they'll just pivot to a helicopter ride-sharing service.”

STV Take: I especially love the landing-the-plane analogy. Landing a plane safely requires a series of steps that begins long before the wheels ever touchdown. This is the whole point of Frank's post—a successful acquisition process begins long before a transaction occurs. It requires founders and investors to be aligned and company operations and financials to be in tip-top shape.

The other point Frank makes is just how many “planes are in the sky” at the moment. The past several years saw many startups get funded that quite frankly will never have the revenue, growth, and margins to be IPO material. For companies with lots of competitors, finding a buyer is going to be a competitive process and founders have to be very clear on the value they bring to a potential acquirer, which again, comes back to being prepared and having clean operations and financials.

🧭 A Guide to Optimizing Financial Performance

AVL Growth Partners released a new guide that highlights the key three financial drivers of a startup, along with recommendations to help founders avoid common financial modeling pitfalls and the best way to project business growth. A few of the common mistakes AVL Growth discusses in this guide include:

Overestimating attainable revenue

Misunderstanding how quickly revenue can grow related to COGs

Underestimating customer acquisition cost

STV Take: Investors understand that a company’s revenue expectations and growth projections presented in a pro forma are educated guesses at best and shots in the dark at worst. Investors can sniff out the latter. While uncertainty is inevitable regarding early revenue growth, there are techniques and best practices founders can use to generate a solid understanding of their cost drivers and present realistic expectations for potential revenue growth. AVL Growth’s latest guide offers valuable tips to help founders craft the best version of their pro forma. (Sponsored)

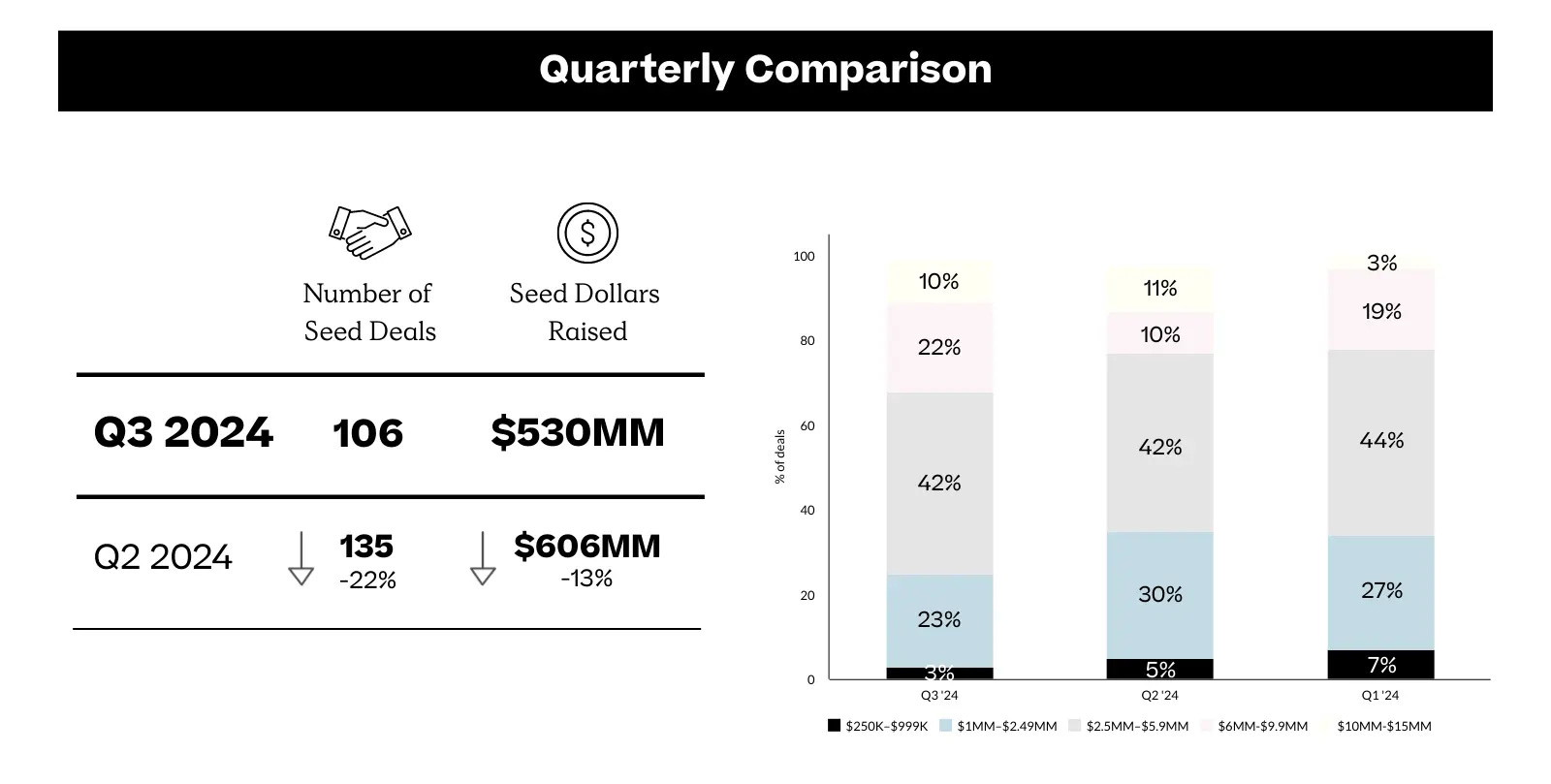

🌃 NYC Seed Report

Primary Ventures released their NYC Seed funding report. Funding to Seed-stage startups in the NYC region declined by 13% from Q2, yet round sizes increased from $4.5M to $5M. In addition to the funding stats, Primary Ventures also highlights thematic trends in funding, including leveraging AI to improve healthcare operations and legaltech.

STV Take: Despite all of the data showing round sizes getting bigger, I am still astounded to see 17 companies raised $9M+ in Seed funding last quarter. As the Primary Ventures team highlights, investors are still trending towards “high-conviction, low-volume approaches”, meaning VC dollars are concentrated in a small number of deals. As I said last week, it will be interesting to watch what becomes of these companies raising giant Seed rounds. For example, will these larger Seed rounds, which in theory should enable Seed companies to achieve more before needing to raise again, eventually shift the revenue needed to raise a Series A higher?

Going back to the first section on harsh fundraising truths, I think it’s important to highlight how exceptional these monster Seed rounds really are. These rounds are likely being done with repeat founders and/or founders with exceptional experience scaling businesses in an adjacent area to what they’re building. For most first-time founders starting their journey, raising a large Seed round is not likely and anchoring on this as a goal for fundraising is only setting up founders for failure.