It’s Not Your Deck That’s The Problem

This week we are bringing you articles on why your pitch deck might not be the reason for no investor interest, the (un)changing Series B market, and insights into repositioning TAM.

Greetings! We are halfway there!

🚨 It’s Your Business, Not the Deck

Builders Field Guide featured an article discussing why a pitch deck’s design might not be the reason for a lack of investor interest. The author, Donna Harris, points out that it usually isn’t about the deck in and of itself, but rather something about the business that is the reason investors keep passing. A couple of the reasons outlined include the following:

Asking for money without proof of demand;

Trying to raise capital for a business that isn’t a fit for venture capital; and

Burying the important information.

STV Take: There is so much fundraising advice out there that is solely focused on deck creation. While a deck is a critical component of the process, it is merely a vehicle for telling the story of why and how a business is going to be the next great company. The big takeaway from this article is that a deck (or raising money) isn’t the first step to building a company. It’s the subsequent step after identifying that venture capital is the right type of financing for the business and early evidence of a potentially fast-growing business has been acquired.

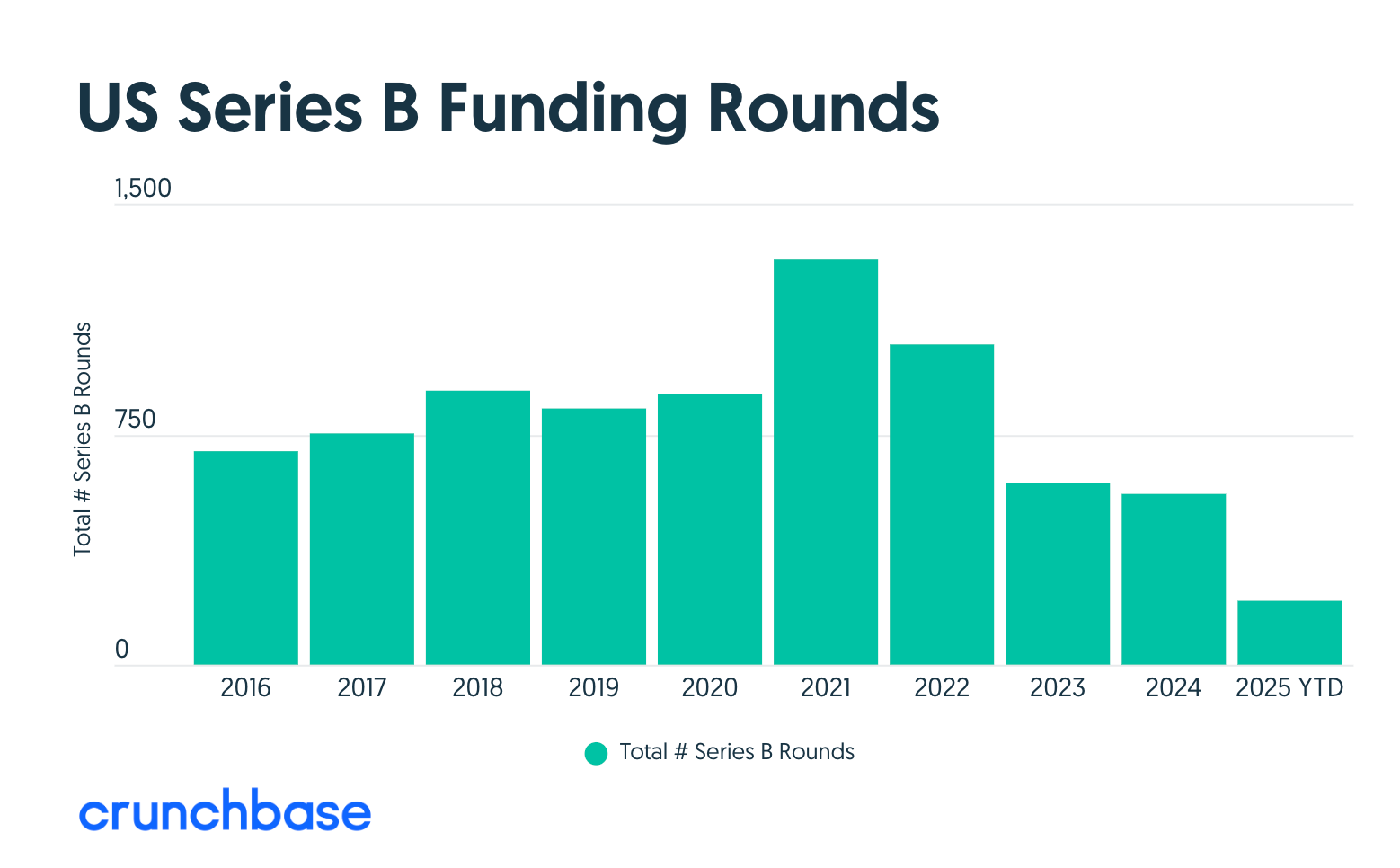

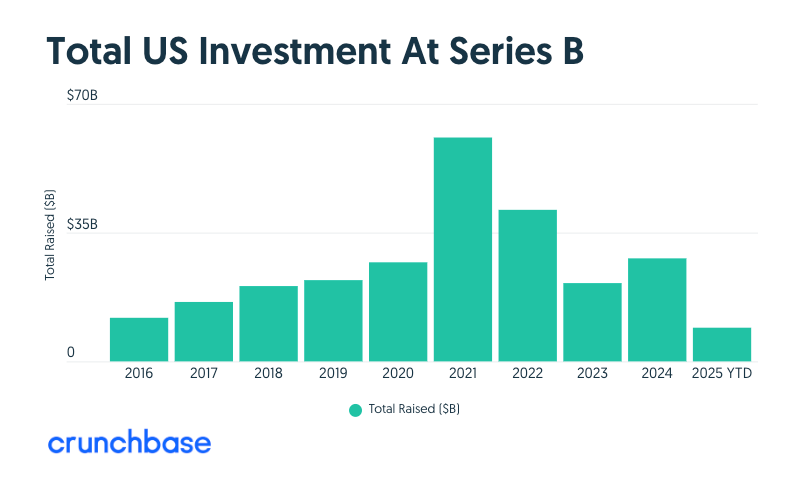

📆 A Decade of Series B Data

Crunchbase released data highlighting the trends in Series B financings that have and haven’t changed. Series B round counts and the ratio of Series A to Series B financings (2:1) are among the things that haven’t changed in the last ten years; however, the total amount of investment into Series B rounds hasn’t been steady, with big increases in 2021 and 2022 relative to prior and subsequent years.

STV Take: There is a lot of discussion lately about how much venture has/is changing, so it’s interesting to see data that shows what has been consistent. What I think has changed is how competitive it is for founders to raise a Series B. This stage has followed the same bifurcation pattern we have seen across Seed and Series A, fewer rounds getting done but at larger round sizes. If you have top-tier metrics, you’re likely going to have your choice of investors, but if not, it will feel nearly impossible.

I wonder how this changes the success/graduation rate of this cohort of companies raising a Series B. Are those raising Series B’s truly the cream of the crop and will success rates reflect that? One of my concerns, though, is that as competition for quality Series B companies heats up, valuations get too high, reducing exit options. I’ve said this a lot, but unfortunately, only time will tell.

🌎 Rethinking TAM

In a LinkedIn post, Anshuman Sinha describes the evolution of his questioning around total addressable market (TAM). Instead of asking founders how big the market is, he asks about the intensely painful problem the company is solving for a niche group. This line of questioning is driven by his belief that great venture-backed companies don’t chase big markets; they create wedges in niche areas that turn into monopolies.

STV Take: Anshuman’s post gets at my beef with most TAM slides, which is that they’re too high-level and general to be useful. Companies have to start somewhere and usually that means finding a very intense, specific problem for a niche segment. Investors love this focus because that means a higher likelihood of really solving a customer’s problem and stickiness, but investors still need to see how the business gets to $100M+ in ARR in <10 years. That means founders not only have to excel at showing how well they solve the problem today but how that wedge drives a bigger market opportunity. Founders need to illustrate a step-by-step progression from their initial focus to increasingly larger opportunities. The more granular a founder can be on that, the easier it will be for investors to see the niche opportunity turning into something bigger.