Same Goal 🎯, New Format

Same Goal 🎯, New Format

We're excited to launch a new Substack format to continue to help founders fundraise better.

Greetings! We’re mixing things up and experimenting with a different take on content. Biweekly, we will use this to (briefly) double click on topics discussed on recent VC Minute episodes and highlight specific content that is best suited for a visual medium (think charts, articles, and images).

💭 Thought Bubble: FOMO → JOMO

In VC Minute episodes 92-96, Damayanti (Dama) Dipayana—who is an absolute powerhouse, by the way; definitely giver her episodes a listen—discusses her experience fundraising for her company Manatee. A key takeaway is that there is a lot of psychology in the fundraising process that first-time founders either don’t know or underestimate (side note: this is why VC Minute exists). As she reflects, one of the things she wishes she’d done better to build conviction with investors is drive FOMO.

FOMO gets mentioned A TON in fundraising strategy conversations (VC Minute episode 39). It’s a powerful tool that should absolutely be in your fundraising arsenal, but it should be used with caution.

At the core, FOMO is largely a perception of potentially losing an opportunity. The reason it can be so powerful is because it appeals to the innate part of us that craves inclusion and is adverse to loss. It creates urgency and a bias to action. For founders, driving FOMO can be the key to building momentum in a fundraising round.

Ideally, you can start to think about leveraging FOMO when you’re advancing conversations with an investor. FOMO can be useful in getting other investors to move their process along quicker. As episode 39 talks about, good investors stick to a decision-making process, meaning they need to have enough time to do the work. When done right, FOMO can persuade an investor to make running that evaluation process their number one priority. If an investor feels like other firms will make a decision before them, potentially precluding them from the opportunity, they will prioritize getting the work done.

What founders get wrong about FOMO is usually a combination of two things, interjecting it at the wrong time and trying to artificially create it. Telling an investor your round is closing in five days on the first call is probably a no-go for most investors, unless you’re a known quantity to the firm. Even then, it’s going to be a stretch. You need to give investors enough time to run an expeditious process by setting a timeline that is far enough in advance to allow them to do this but also forces them to push this to the top of the stack.

Trying to build artificial FOMO by outlining a tight timeline with little to none of your round committed can, and likely will, backfire. Throughout the diligence process, investors are assessing and getting to know you. Credibility, transparency, and solid communication are all traits VCs are looking for in founders. If an investor feels that the timeline was feigned in an effort to create artificial FOMO, it will come across as deceitful, manipulative, and/or desperate. Investors understand closing dates get pushed and things don’t always come together as nicely as everyone hopes, but if high-pressure tactics have been used to get folks to commit by a certain date and that time comes and goes without most of the round accounted for, it doesn’t look good on the founder. Trust is one of the most valuable assets, and once that has been broken, the damage is done.

The takeaway is that FOMO would have worked in Dama’s situation because she had committed investors and a few other very interested potential investors. It isn’t effective when founders force a quick decision timeline without having any real investor interest. That’s when FOMO runs a very real risk of turning into JOMO (the joy of missing out).

📖 Market Report

Carta released “State of Private Markets: Q1 2023” earlier this week, and it’s definitely worth a read. Not surprisingly, venture capital investment dropped and is the lowest it’s been since 2017.

and total cash raised (line) by quarter, Q1 2016-Q12023")

Some other highlights from the report:

20% of investments done in Q1 were at valuations less than the previous round, AKA a down round. This figure was 5% a year ago.

>25% of states in Q1 had no companies receive a venture capital investment.

The median time between raising a Seed and Series A is now 678 days.

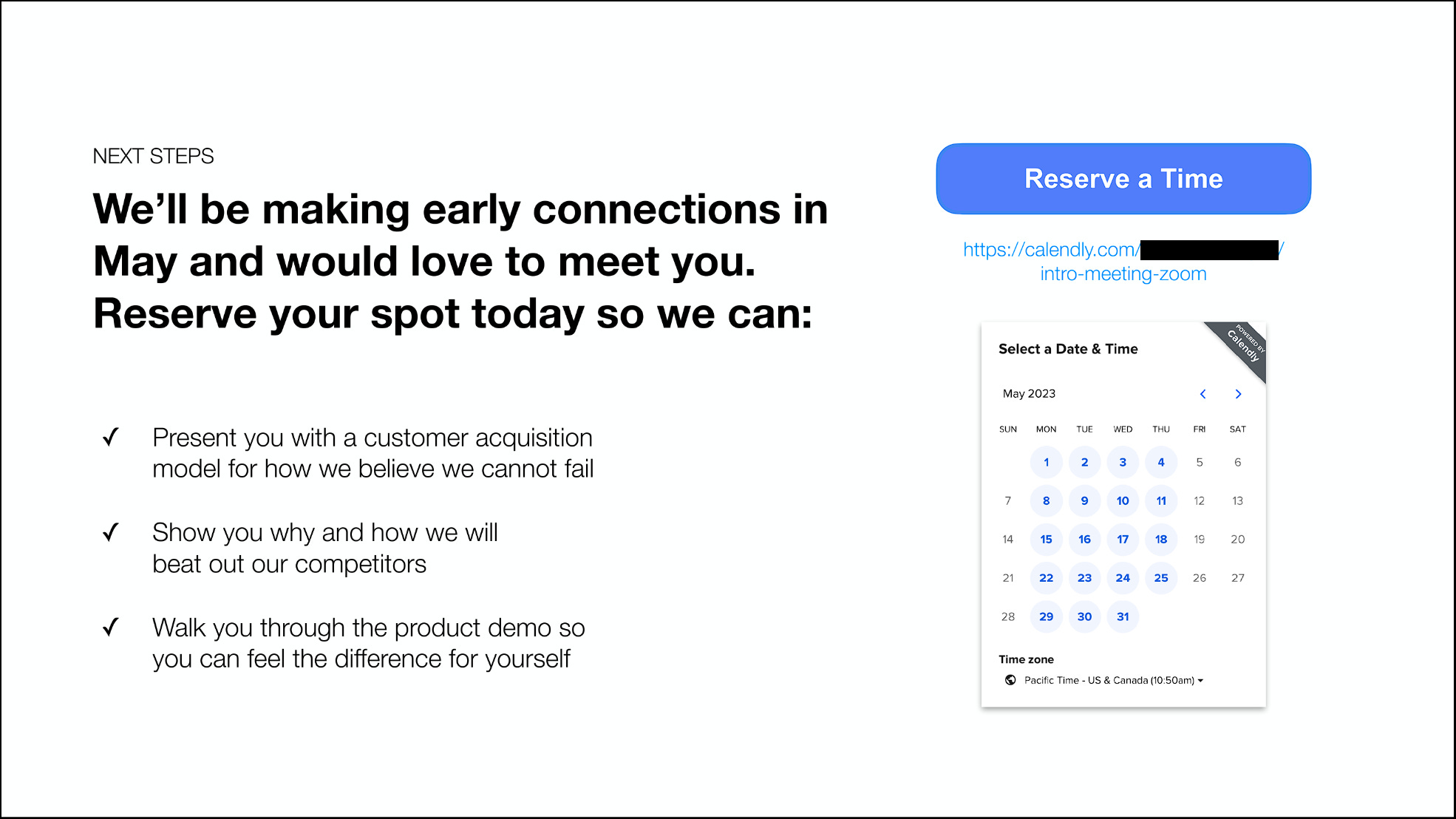

💡 Slide of the Week

More often than not, slides leave a lot to be desired. That’s why when we see an exceptional one, we think it’s worth calling out here.

What is great about the slide below is that it contains the following:

A clear call to action: scheduling an intro Zoom,

A frictionless way to take that action: linking to a scheduling link (see Ep. 027),

Details on why the reader should take that action: the what’s-in-in-for-them question, and

It’s novel: founders rarely, if ever, do this.

😴 Decompression Zone

Building a business is a marathon, not a sprint. It’s important to practice self care (VC Minute’s self-care compilation here), and this adorable puppy, Sam, is your reminder to carve out time for yourself.

That’s it! We hope you enjoyed this new format, and if you have thoughts on what you’d like to see here, let us know.

Thank you for your time, and have a great week! 👋