Startup Postmortem

This week we are bringing you two reports and a founder's honest evaluation on why their startup failed.

Greetings! That was quite the Winter Olympics 🎿 🏔️

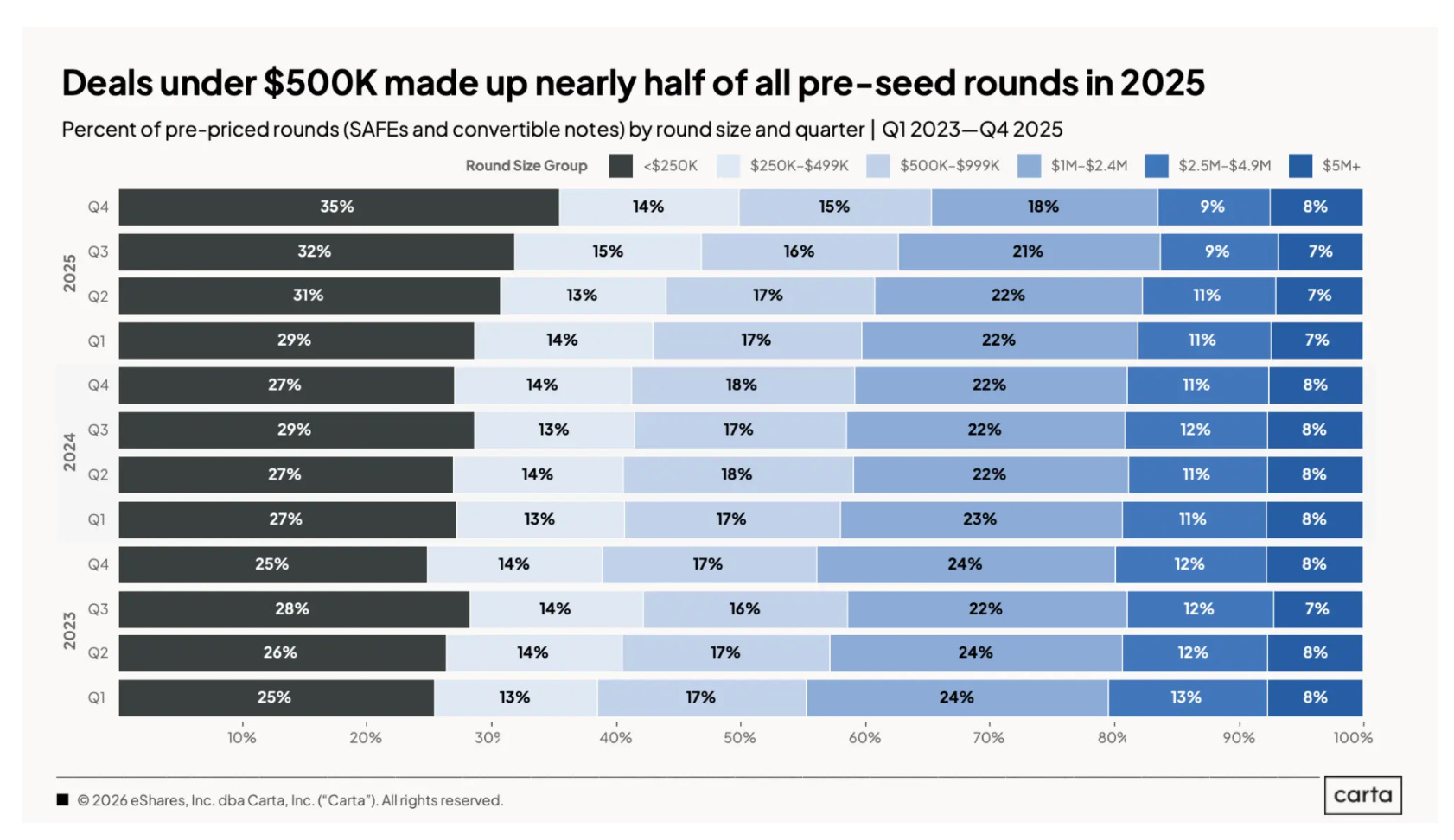

📊 State of Pre-seed 2025

Carta released their full report featuring data and trends at the Pre-seed funding stage, which Carta defines as “any fundraising activity that occurs on convertible instruments prior to a company’s first priced equity round.” Much like every other stage of financing, capital is consolidating into fewer deals. While just 1% less capital flowed into Pre-seed deals in 2025 compared to 2024, it went into 13% fewer companies.

STV Take: This report drives home just how bifurcated the Pre-seed market is. Roughly half of companies are raising <$500K at their first round, while 8% are raising $5M+. What is most interesting to me is the hollowing out of the $250K to $2.4M range. That has dropped by at least a couple of percentage points since 2023; e.g., 10% more rounds are for less than $250K. What this really emphasizes is that founders need to be more intentional than ever about how much they raise and what they can prove with it. A smaller check isn’t disqualifying, but it does compress the margin for error, making focus and milestone clarity critical from day one.

💔 A Startup Postmortem

Rachel Draelos, MD, PhD spent seven years building Cydoc, a bootstrapped health AI startup focused on automating patient intake and clinical documentation, before shutting it down in August 2025. Despite achieving what she thought were real validation milestones (e.g., paying customers, patents, and demonstrated clinical time savings), the company ultimately couldn’t overcome a broken business model. In this article, Rachel reflects candidly on the nine key mistakes she believes she made trying to build Cydoc into a successful business. A few from the list include inadequate sales and marketing, not having the right cofounders, and minimal customer discovery.

“We wasted years, tens of thousands of dollars, and many person-months of labor building features that customers didn’t want, and leaving out features they desperately needed.”

— Rachel Draelos, MD, Ph.D.

STV Take: This is a rare gem because of how candid it is. We’ve touched on many of the issues Rachel raises, but it cuts differently when it comes from someone who recently had to shut their company down because of them. Her piece brings to life why VCs fixate on certain risks. These are not abstract criteria to investors, because they’ve seen these exact patterns play out. When you’re raising, a lot of advice gets thrown your way, and not all of it deserves equal weight; however, if a particular concern keeps coming up across multiple investors, it’s worth pausing. Chances are investors are pattern matching against a mistake they’ve seen before. Rachel’s article is a good lens for figuring out which feedback falls into that category.

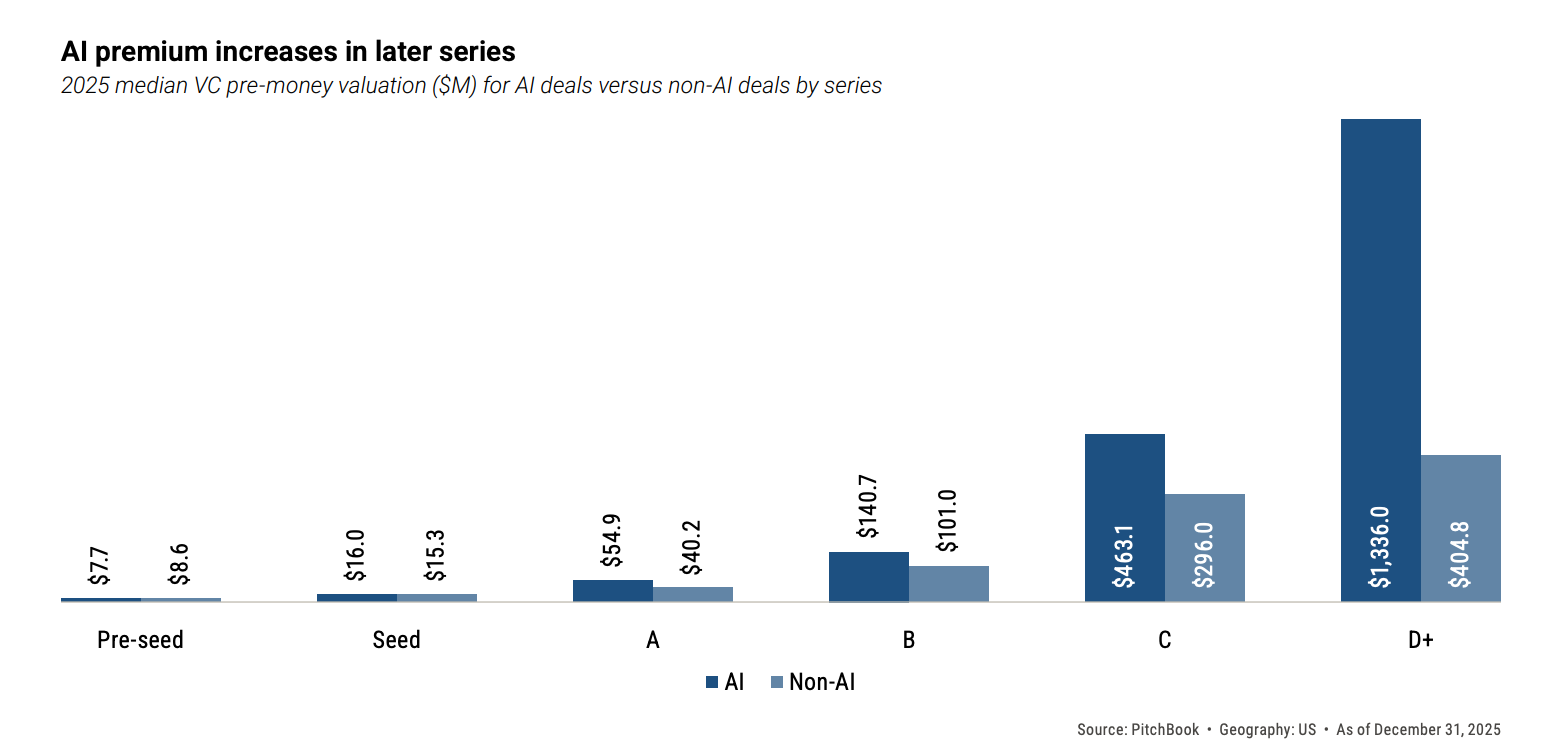

💰 U.S. VC Valuations and Returns Report

Pitchbook released a report on valuations in the U.S. venture market. Unsurprisingly, it shows venture concentrating into a handful of perceived winners, generally in AI. A few interesting data points from the report:

20.9% of rounds in 2025 were at valuations that were flat or less than the prior round.

Top-decile valuations at the Series B have increased by 64% in 2025 relative to 2024.

The media pre-money valuation for a Seed-stage AI company is $16M, while the median pre-money valuation for a Seed-stage non-AI company is $15.3M. This disparity only grows in subsequent rounds (see chart below).

STV Take: One of the more interesting facts Pitchbook calls out is the current status of U.S. unicorns. According to the report, there are 857 unicorns; however, on average, these companies have not raised a fresh round of capital in 2.5 years ago. Because of the length of time since the last round and change in market dynamics, Pitchbook estimates that about a quarter have actually had their valuations dip below $1B since their last round.

This matters to founders fundraising at Seed because the slowdown at the unicorn stage doesn’t stay contained there. With many late-stage companies sitting on stale valuations and limited liquidity, distributions back to LPs have slowed. That has made it harder for VC firms to raise new funds, particularly emerging managers who disproportionately invest at pre-seed and seed. The result is a tighter early-stage funding environment: fewer new funds coming online, smaller fund sizes, longer decision cycles, and a higher bar for conviction. For seed founders, this means investors are writing fewer checks, reserving more for existing portfolio companies, and underwriting more conservatively than they did in 2020–2021.