The Dangers of Playing it SAFE

The Dangers of Playing it SAFE

How frequently are SAFEs used in early-stage rounds? What’s the risk of stacking SAFEs? Why are there less publicly traded companies?

Greetings! We are back with another set of resources to help answer these questions.

Just a reminder, SpringTime will be hosting a webinar, titled “SEED CRUST: State of the Seed Market”, tomorrow, May 2nd, from 1-2pm ET. We’ll cover the market forces that are keeping startups stuck in the Seed phase, discuss paths forward, and share some rays of sunshine. We’ll also be joined by special guest, Peter Walker, Head of Insights at Carta.

RSVP here.

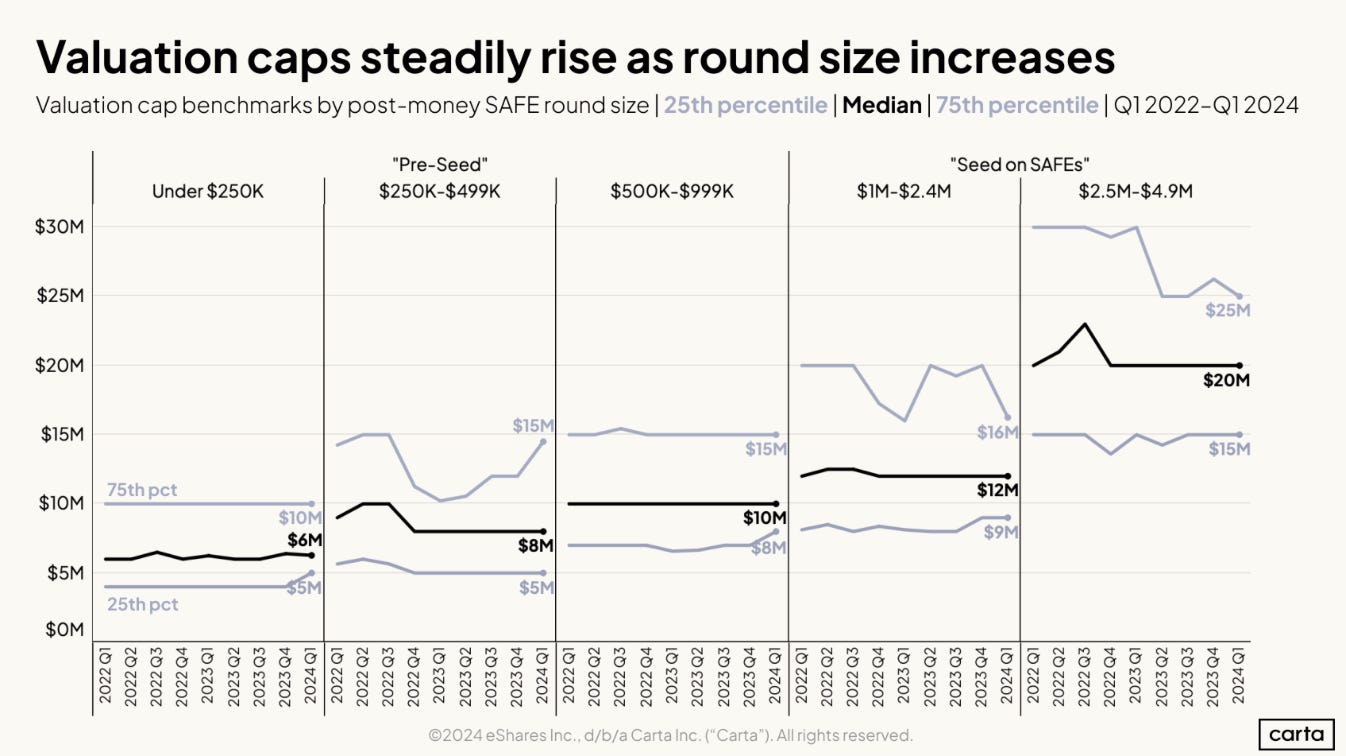

💸 State of Pre-Seed: Q1 2024

Carta’s latest report, State of Pre-Seed: Q1 2024, discusses the trends in Pre-seed rounds, which as Carta notes is a bit of an ambiguous term and part of what they hope to demystify through this report. Interesting stats include:

Investments made into companies on SAFEs and convertible notes; i.e., prior to a priced round, is roughly flat compared to Q4 2023.

72% of pre-priced rounds were for round sizes less than $1M.

The SAFE was the convertible instrument of choice for 88% of companies that raised a pre-priced round.

Notable Highlight:

STV Take:

The difference between Pre-seed and Seed is, as mentioned, often obscure. There are big differences in round dynamics between companies raising $250K and $1M+, and this report does a great job of starting to suss those out. It also contains good benchmarks on what is standard around discounts, caps, and expected founder dilution based on caps.

😱 Fundraising Fundamentals: Stocking Stuffer SAFEs

In this article, First Mile Ventures highlights the ramifications of raising multiple investment rounds on convertible instruments, which include more expensive legal fees at the priced round and dilution.

Notable Highlight:

“Sometimes, you need to do whatever is necessary to raise capital and keep moving, but it’s important to keep the end goal in mind and understand the long-term impact of those short-term decisions.”

STV Take:

As the Carta report noted, SAFEs are still the preferred instrument for raising money at the earliest stages. It obviously doesn’t make sense to avoid them entirely but managing them is critical. We mentioned the potential impact of SAFEs on founder dilution in our prior newsletter, but it is a point worth reiterating as companies stay in the Seed phase longer. Fortunately, Carta has a free calculator tool that allows founders to run scenarios on the impact of convertible instruments on dilution.

😕 Where Did All the Stocks Go?

Chartr had a super interesting write-up on an academic paper discussing the decline in the number of publicly traded companies in the US. In it, the Chartr authors provide context on the various theories that have been floated to explain this decrease before ultimately identifying M&A as the primary cause.

Notable Highlight:

STV Take:

One of the potential reasons discussed for this decline is that companies are staying private longer. While most VCs will hold their position in a company for several years, at some point they will need to see liquidity, which usually happens through either an IPO or M&A. This need, which for later-stage companies can often only come from the deep pockets of the public markets, means that eventually companies will have to go public. Companies staying private longer just slows the pipeline down; it doesn’t eliminate it.

M&A as the culprit for this decline can be either good or bad, depending on which side you’re on. If you’re a founder, an acquisition from a leading company can be life changing, and as the article points out, if you’re an existing shareholder in the acquirer, it’s also probably good for you, as value continues to accrue to that business rather than what could have become a competitor. If you’re a VC, on the other hand, an acquisition might be a fine outcome but not necessarily one that will meaningfully drive fund returns (VC Math ≠ Founder Math).