The Dangers of Stacking SAFEs

This week we cover articles highlighting the potential pitfalls of stacking SAFEs, common pitch deck mistakes, and when profitable companies should pursue VC funding.

Greetings! If you’re in the U.S., we hope you had a great Memorial Day!

📚 Stacking SAFEs

Peter Walker posted data on LinkedIn about the number of companies on Carta that have stacked SAFEs; i.e., raised money on multiple SAFEs at different valuation caps. In the post, he outlines the pitfalls for both founders and investors, which are that SAFEs can be surprisingly dilutive for founders and investors can lose track of how a company is progressing. Peter recommends that after one or two SAFE rounds it’s time to clean it up and do a priced round so everyone knows what they own.

STV Take: Unfortunately, over the years, we have seen the implications for founder ownership of stacking SAFEs and the founder’s surprise that usually accompanies it when the SAFEs are finally converted. One of the interesting discussion points that gets brought up in the comments section of the post is how much this SAFE stacking is attributed to “kicking the can down the line” for a priced round. I actually think that is a likely explanation. As the metrics needed to raise the next round have increased, more companies are doing bridge rounds and potentially doing those on SAFEs at slightly higher valuations than the last one to give some credit where progress has been made.

The other piece to this that we sometimes see is where founders will raise an early round and use different valuation caps based on when investors commit. Generally, we are not fans of this practice. Sure, it can drive urgency to get investors to commit early, but it can also create some awkward, trust-losing interactions, especially if the round doesn’t come together as the founder anticipates. It just overly complicates a round if all investors are committing within a month or two of each other.

🤨 10 Common Pitch Deck Mistakes

In a recent YouTube video, the Deck Doctors outline the top pitch deck mistakes they frequently see and examples of how to fix them. A few of the most common offenders include the following:

Bad images, including those that are AI-generated and stock photos that look like relics from the aught years;

Too much text; and

Competition slides that only list features.

“For an investor pitch, we don’t really care that much about hand-picked features that you’re clearly going to check the box on.” — Deck Doctors

STV Take: The points discussed around competition are worth reiterating. Most categories are becoming increasingly competitive, so listing a bunch of cherry-picked features does little to move an investor reading the deck. Instead, leading with where gaps are in the market and how a specific insight opens up a market is much more compelling. This is even more important as AI gets better at generating code. No matter how much you believe (or don’t) the AI hype, the question top of mind for most investors now is how you build defensibility in a world where AI makes it so much easier to build.

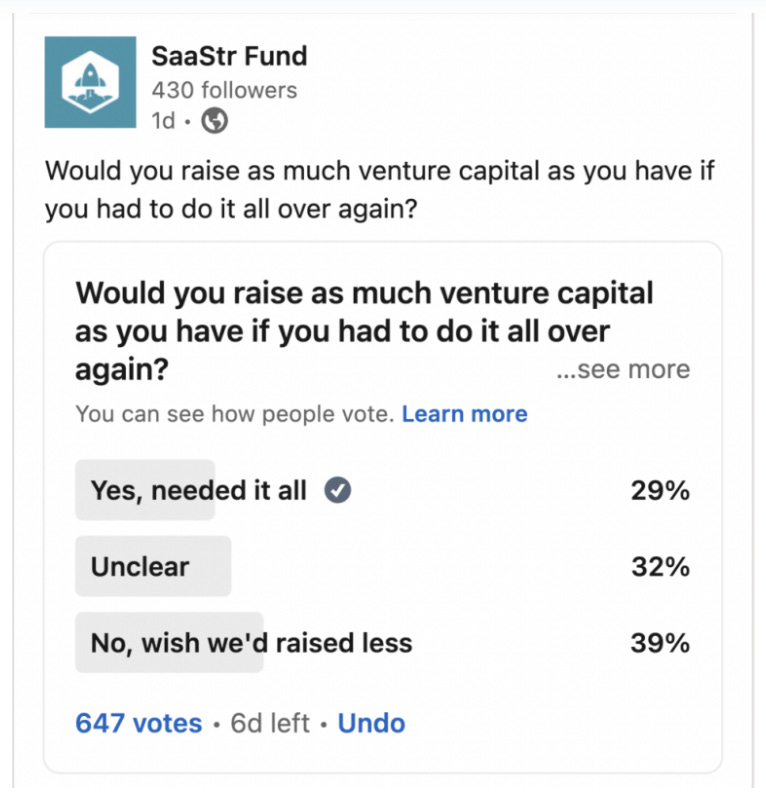

🧐 Raising VC for a Profitable Business

In a recent “Dear SaaStr” article, Jason Lemkin answers the question of when profitable businesses should consider taking on VC capital. Jason advises that founders should consider this capital when they need to strengthen the balance sheet ($1 in balance sheet capital for every $2 in ARR is Jason’s recommendation) and know where to spend it. It’s likely not worth it if you can’t put the money to work in a meaningful way.

STV Take: The advice provided in this article is applicable regardless of where you’re at in your fundraising journey. Getting bombarded with investor interest is not uncommon after a fundraising announcement, and it’s important for founders to recognize when these inquiries might be a distraction. It’s easy to get caught up in potentially more money, but the SaaStr X survey (image above) provides a dose of reality that raising more VC capital isn’t the panacea and comes with its own strings. If there isn't a clear, useful path for VC funding, it’s likely not worth exploring.