The Sins of Pre-seed Fundraising

This week we bring you Pre-seed fundraising tips (a.k.a. what not to do), a venture arrogance score, and insights into why secondaries are the saving grace for early-stage fund managers.

Greetings! What a week of nasty weather! ⛈️

🙈 12 Deadly Sins of Pre-seed Fundraising

Sam Awrabi, Managing Director at Banyan Ventures, posted the 12 common mistakes he sees founders make when trying to raise a Pre-seed round of funding. Some relate to VC outreach and how to run a process—such as including a link to a pitch deck and having a basic data room—while others are more about content and communication.

STV Take: The first (never slow down sales to fundraise) and the last (lack of understanding of competition) points are particularly worth driving home. Pre-seed is evolving and many investors are expecting some level of traction. The days of being able to raise a Pre-seed on an idea are gone. While many Pre-seed investors might not require revenue, they still expect to see momentum building with customers. Pausing the sales process not only sends a negative signal of a founder’s potential to manage multiple tasks but also hinders the ability to continue to show progress as fundraising conversations evolve.

On the last point around competition, investors know competitive landscapes can change overnight. We won’t ding you for that; however, not understanding the scope of competition, which might just be inertia, does send a poor signal. Investors want to know why the product is 10x better than what’s out there and why customers will be willing to make the switch.

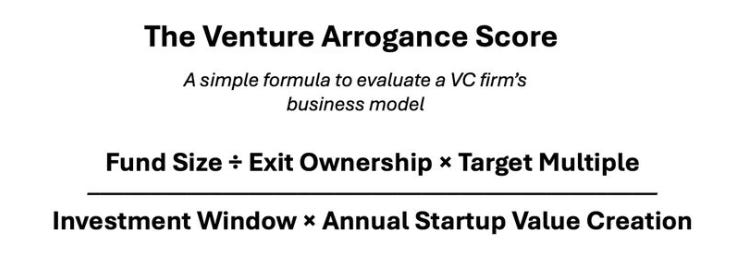

🎲 The Venture Arrogance Score

On a recent episode of the podcast, Uncapped, host, Jack Altman, interviews Josh Kopelman, co-founder of First Round of Capital, to get his take on the current state of venture. The discussion starts with Josh making the bull and bear cases for the larger $1B+ funds that have cropped up in the last couple of years. The conversation then segues into how larger fund sizes often drive more visibility, and consequently, better access to deals. However, this can be short lived if funds don’t find enough success to keep them going. Tiger and SoftBank are used as examples. Lastly, the conversation turns to First Round Capital and how they run their firm like a company, focused on building what they see as their product, their decision making process.

STV Take: This is a fascinating, detailed look into fund math and how firms raising very large funds may or may not be able to 3x their fund. I’m not sure I agree with Josh’s point that whether or not these funds are successful doesn’t really matter to founders; new capital will just plug the hole, much like what happened with Tiger and Softbank. While I don’t have a crystal ball, I do think at some point liquidity, or lack thereof, will have profound ramifications, especially for those larger funds. Either the case will be made that exits are larger than they ever have been and thus warrant all of the additional private capital that’s poured into them… or it won’t. I don’t know when that time comes, but I absolutely think founders should have a pulse on how venture is evolving and the different incentives that different investors have. If nothing else, it helps them understand the requirements they’ll be held to if/when they decide to fundraise.

🙏 Thank Goodness for Secondaries

Hunter Walk at Homebrew penned an article discussing how and why secondaries are becoming more and more important for Seed-stage fund managers. Specifically, with companies staying private longer, what used to be a 7-10 year journey from a Seed investment to a liquidity event is now closer to 10-12 years. This has real implications for calculating the internal rate of return (IRR), which at a very basic level is the compound annual growth rate of an investment. Because of these longer hold times, along with more infrastructure and acceptance around secondaries, Seed-stage fund managers are seeing secondaries as a critical path to generating liquidity.

STV Take: With few IPOs on the horizon and uncertainty around when, and even if, it will pick back up, many early-stage investors are looking towards secondaries as a way to bring some much needed liquidity to their limited partners (LPs). No matter how convicted a Seed-stage investor is in a company, at some point, early investors will eventually need an out. Secondaries are emerging as a way to do just that. As more and more of these transactions happen, stakeholders are getting comfortable with the idea of selling a portion of a stake in a company. We talk a lot about how venture is changing, and nowhere is that more apparent than the buzz around secondaries. If you’re a founder raising Pre-seed and Seed capital today, it won’t surprise me if secondaries are fairly expected and standard by the time you raise a Series B.