VC Dealmaking Indicator

This week's featured topics include a financial model template, an indicator of startup fundraising conditions, and insights into company valuations.

Greetings! We are halfway through the week and nearly halfway through March—it’s going fast!

✏️ SaaS Financial Model Template

SaaStr featured an updated financial model template from Christoph Janz, Managing Partner at Point Nine Capital. The updated version allows for multiple pricing tiers, annual contracts with prepayments, (more!) charts, and better visibility into cash flow. Of course, every business is different so this template is best used as a starting point, with founders tailoring it to their own unique needs.

“I’ve seen terrible [financial models]. I’ve seen 100% Gross Margins. I’ve seen terrible misunderstandings of the differences between MRR, ARR, and revenue.

Get help. Get at least an outsourced controller that has done SaaS.”

— Jason Lemkin, Founder, SaaStr

STV Take: I concur with Jason. I am never surprised by the financial pro formas I receive. Pre-seed and Seed-stage investors know that projections at the earliest stage of a business are, for lack of a better term, guesses. There are so many moving pieces and revenue isn’t predictable, but they’re critical for raising capital, especially at the Seed stage.

So, why build a pro forma if investors know it will change? First, it’s a good exercise for founders and investors to see how the money flows and understand the key levers to the business. Second, it’s a great way to pressure test assumptions about revenue growth. Essentially, a good pro forma tells the detailed story of revenue growth.

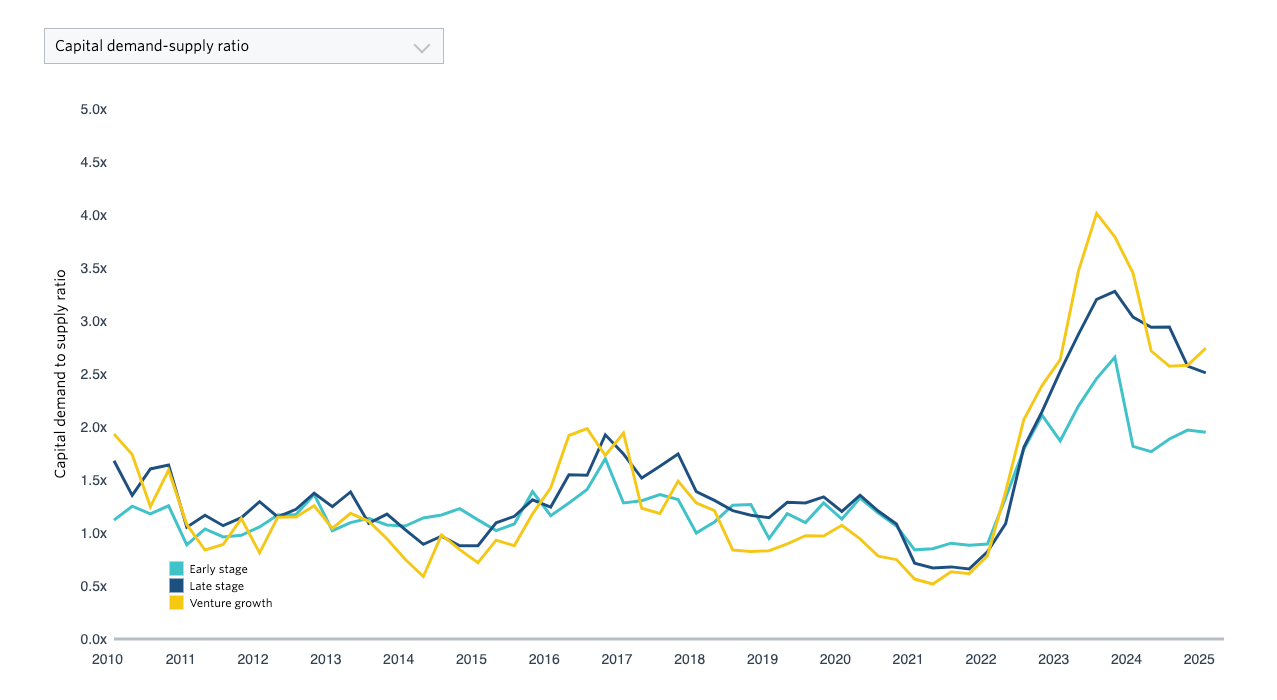

🌡️ VC Dealmaking Indicator

Pitchbook released their latest VC Dealmaking Indicator, reflecting the state of the market from the perspective of investors and startups. Not surprisingly, the market favors investors, which has been the case since 2023.

STV Take: Also included in that report is the above chart, which shows the amount of deployed capital relative to the startup demand for capital that is part of the calculation for determining the dealmaking indicator. While I have questions around the methodology of how they determine demand, this chart is fascinating nonetheless. At every stage, the amount of demand for capital far outstrips the supply at historical levels. I’d love to break down the early-stage category even further, but that wasn’t possible. No matter how you slice it, though, I suspect it’s the same: the competition for capital has never been fiercer.

🧮 The Valuation Calculus

On LinkedIn, Alejandro Cremades shared a link to a presentation by Mercer Capital that discusses what goes into determining a startup’s value. While the linked presentation is several years old, it’s still a good resource for founders looking to understand the various nuances that go into valuing a company. For Alejandro, the three key takeaways from the report are the following:

A startup’s stage matters.

There are multiple ways to value an enterprise.

There is a risk-reward component to the assessment. There are always deviations, but in general, the higher the risk, the lower the valuation.

STV Take: As most readers of this newsletter know, determining a company’s valuation at the Pre-seed and Seed stage is based more on standard market norms, like typical founder dilution at that stage of funding, than pure metric-driven analysis. However, as we have discussed, eventually, the valuation must align with the business fundamentals, which the overview Alejandro links to is a good window into what that assessment actually looks like.

Every Seed investor knows that their portfolio companies will eventually undergo this analysis and factor that into their decision-making process. Knowing the ins and outs of how a later-stage company is valued is just another way for founders to understand what might be running through an investor’s head when they balk at valuation. Of course, the caveat to this is that not every investor is disciplined and logic can go out the window if the deal is hot.