Venture Capital 101 🎒

This week we are bringing you a fresh fundraising playbook, an article series designed to serve as VC 101, and insight into how funds are evaluated (more of a 201 topic, honestly).

Greetings! Whoa, has it felt like spring! 🪻🌸

🎓 Intro to Venture Capital 101

In the introduction to a new series of articles called “Venture 101”, Stanford GSB professor Ilya Strebulaev sets out to explain venture capital mechanics in plain English. He previews future topics including preferred stock, SAFEs, convertible notes, governance, control rights, and follow-on rounds, but starts with a walk-through of how venture financings work. The post is designed to help founders better understand the mechanics behind selling equity before they are negotiating terms in real time.

“...the critical feature of a SAFE is its conversion into the security the startup will issue later on, and without knowing that security it is tough to understand SAFE properly.”

— Ilya Strebulaev

STV Take: We think this is the kind of content founders should review before the term sheet shows up. You do not need to become an expert in venture finance, but you do need to understand enough to know where the economic and governance tradeoffs actually sit. The reality is that some of the most important decisions in a financing are easy to gloss over when you are focused on simply getting the round done. Founders who do a little homework ahead of time can save themselves a lot of time and headache once the pressure of a live raise sets in.

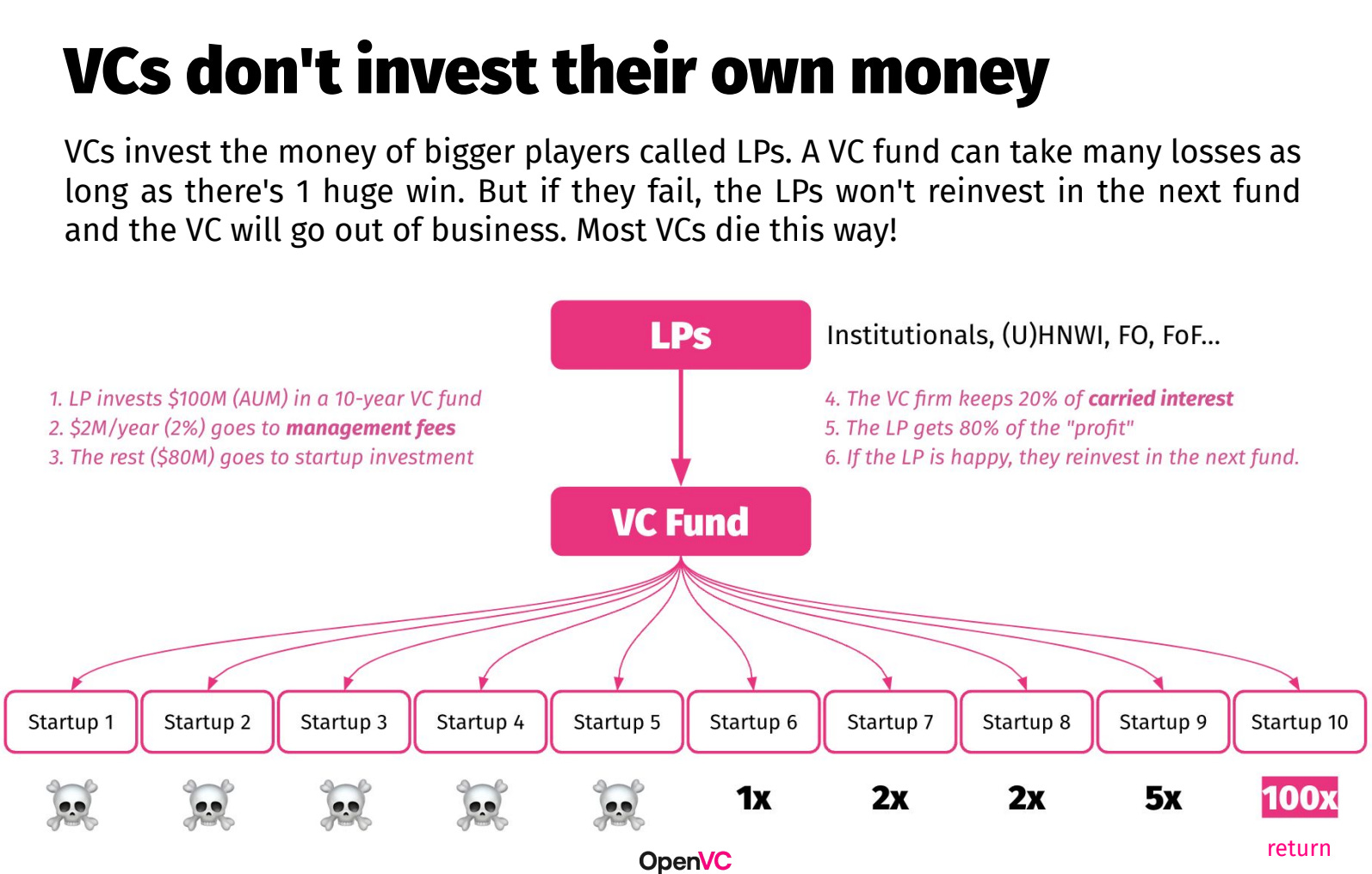

🧰 2026 Startup Fundraising Playbook

OpenVC published a practical playbook designed to help founders run a more structured fundraising process. The guide walks through how venture capital works, fundraising strategy, investor targeting, materials preparation, valuation, and process management. It is broad, but intentionally tactical, with the goal of helping founders more efficiently manage their raise. For founders who have not raised before, it is a useful starting point.

STV Take: The above image is a good primer for our next article, but this whole playbook is great because it treats fundraising like a process to be managed rather than a mystery to be solved. Too often, founders start taking meetings before they have built a target list, pressure-tested their narrative, or thought through how to create momentum. When fundraising is unstructured, every conversation can feel more promising than it really is. A thoughtful process helps founders better separate real traction from false starts.

📊 A Framework for Benchmarking Private Investments

This (oldie but goodie) Cambridge Associates piece explains how institutional investors evaluate private investment performance and why no single metric tells the full story. It covers IRR, time-weighted returns, cash-on-cash multiples, and public market equivalent analysis, while also noting that private funds often take years to settle into their ultimate performance quartile. The article is written for an LP audience, but it offers a useful view into how venture funds themselves are judged.

“On average, a fund needs about six years to ‘settle’ into its final quartile ranking versus peers. Funds can shift significantly among quartiles, with 80% to 90% of funds landing in at least three different quartiles through the course of their lives.”

— Jill Shaw, Partner, Cambridge Associates

STV Take: Founders often spend a lot of time trying to understand how a VC evaluates their company, but less time thinking about how that VC is being evaluated by their investors (limited partners, LPs). This piece is a good reminder that VC fund managers operate in a system where performance is noisy, slow to reveal itself, and constantly benchmarked against peers and public markets. Understanding the venture capital chain is critical and can make VC behavior look a lot less arbitrary. After all, unless they are investing only their own money, venture capital fund managers are answering to someone too.