Vertical & SMB SaaS Benchmarks

This week we are highlighting articles on the data behind Vertical SaaS company expansion, founder dilution, and the lengthening road to Series A.

Greetings! We hope you’re having a great week.

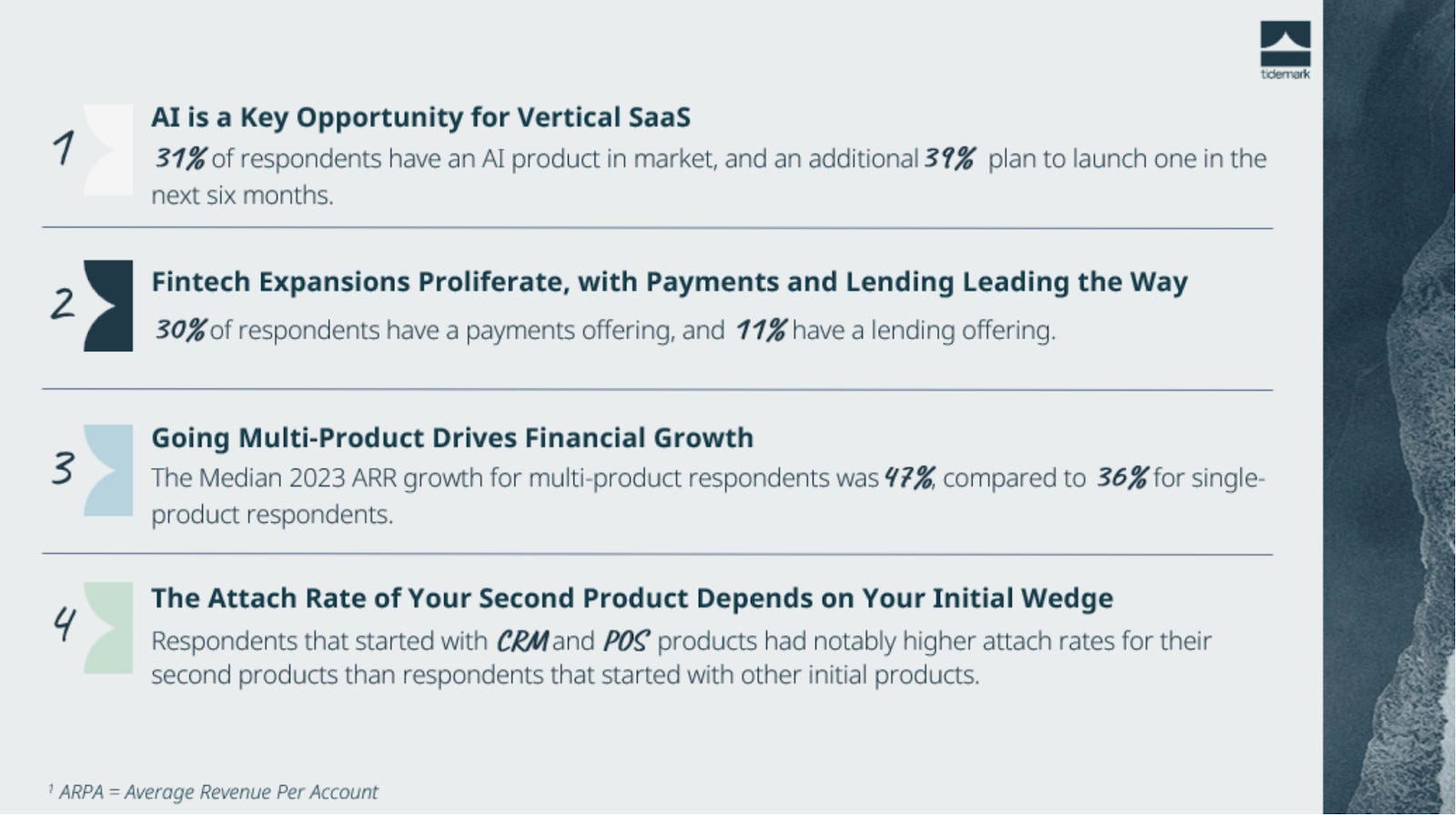

🎯 2024 Vertical & SMB SaaS Benchmark Report

Tidemark released a report with data on benchmarks for topics including retention profiles and product attach rates for Vertical SaaS tools, along with a useful framework to think about expansion. The framework consists of four key parts—winning a critical part of the business (e.g., back office or employee management), scaling across multiple locations, offering additional products, and moving across the value chain.

STV Take: One of the intriguing parts of this report is the breakdown of different “control points”; i.e., the most critical parts of the business, and the difference in median average revenue per account (ARPA) for solutions across these areas. Of the five control points listed (fintech, commerce, back office, employee management, and other), fintech had the highest median ARPA. The lowest—by quite a bit—was commerce, which the report describes as the tools that bring in customers. This starts to shed some light on why many investors are keen on certain Vertical SaaS solutions, like fintech, relative to others. The revenue opportunity is just larger.

One of the significant challenges for Vertical SaaS founders, especially those focused on SMBs, is telling a compelling story about how the business will achieve venture-scale growth when raising capital. For early-stage founders, this report can be useful in considering expansion strategies and crafting a narrative that builds investor confidence in the opportunity.

🧮 Understanding Dilution

A.T. Gimbel at Atlanta Ventures published an article for founders needing a foundational understanding of basic dilution and the various things that can impact what a founder ultimately receives at exit, such as SAFEs and liquidation preferences. The article also includes a link to a basic template to help founders conceptualize the impact of a financing on a founder’s ownership.

“I also encourage entrepreneurs to not just model the impact of a current fundraising round, but also any projected future rounds to make sure you understand the path you are going down.”

— A.T. Gimbel

STV Take: This probably doesn’t need to be said, but it’s so critical for founders to understand the impact of financing on their ownership before any investment is taken. Doing a priced equity round presents a fairly straightforward outcome for ownership; however, the earliest financings of a company are usually done on a SAFE or convertible note, which can create ambiguity on how much a founder owns. In our experience, the trouble usually arises from stacking SAFEs, meaning raising capital on multiple SAFEs with different valuation caps. Using a tool, like Carta, can help you keep track of issued SAFEs and prevent an unpleasant surprise when a priced equity round is finally done.

🗺️ A Guide to Optimizing Financial Performance

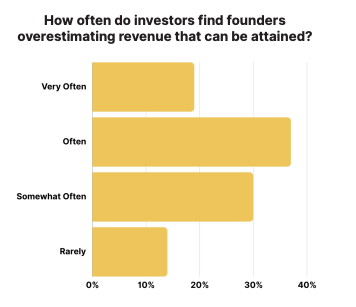

AVL Growth Partners released a new guide that highlights the key three financial drivers of a startup, along with recommendations to help founders avoid common financial modeling pitfalls and the best way to project business growth. A few of the common mistakes AVL Growth discusses in this guide include:

Overestimating attainable revenue

Misunderstanding how quickly revenue can grow related to COGs

Underestimating customer acquisition cost

STV Take: Investors understand that a company’s revenue expectations and growth projections presented in a pro forma are educated guesses at best and shots in the dark at worst. Investors can sniff out the latter. While uncertainty is inevitable regarding early revenue growth, there are techniques and best practices founders can use to generate a solid understanding of their cost drivers and present realistic expectations for potential revenue growth. AVL Growth’s latest guide offers valuable tips to help founders craft the best version of their pro forma. (Sponsored)

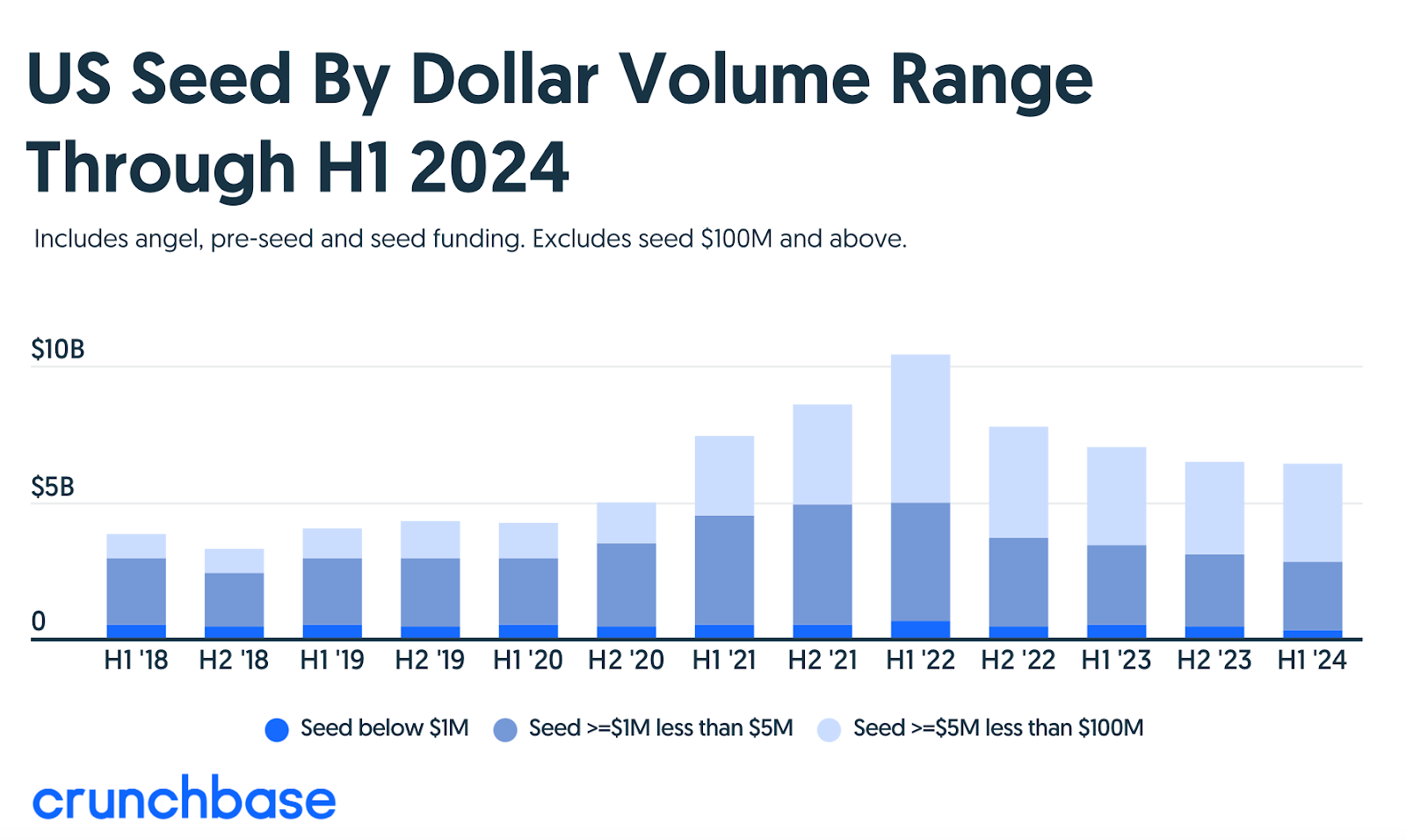

🛣️ The (Longer) Road to Series A

Crunchbase has released new data that highlights a trend we've discussed before: the extended path to Series A. The Seed stage now encompasses a range of companies, from pre-seed and pre-revenue to those nearing $1M in revenue and raising a third round of funding. Similar to other reports, despite the challenging fundraising environment, Seed round sizes and valuations remain stable.

STV Take: While this may not be new information, it’s useful to examine the data behind the anecdotes about the challenges of raising a Series A in the current market. As the bar for Series A funding has risen, Seed round sizes have also increased as companies seek to extend their runway. Not every company can or should raise a large Seed round, and although constant fundraising is less than ideal, a more modest Seed round might actually be beneficial. Limited capital can foster focus, and with investors increasingly valuing capital efficiency, a large Seed round leaves less room for error if the founder doesn’t succeed on the first attempt.