What Does It Mean to be Venture Backable?

This week we feature articles on assessing whether VC is right for your business, how much equity is typically given up at each stage, and how early-stage companies are "leapfrogging" to compete.

Greetings! We hope your week is off to a great start!

🧐 Is Your Business Venture Backable?

Carolyn Witte and Leslie Schrock co-published the first article of a three-part series discussing if, when, and how founders building women’s health companies should raise venture capital. In this first article, Carolyn and Leslie outline the following seven questions founders should ask themselves before fundraising and the types of answers that indicate whether raising VC might be appropriate:

Is the market size in the billions?

How quickly can revenue grow?

Can meaningful growth occur without costs growing linearly?

Does the tech improve the margins?

Who pays and how much?

Is the product and approach truly differentiated from what’s out there?

Why now?

Notable Highlight: “Fundraising is time and soul sucking, and every minute you spend chasing the wrong money is a minute wasted versus building your business.” – Leslie Schrock

STV Take: While the article is geared for founders of women’s health companies, the high-level takeaways are relevant no matter which space you’re building in. Raising venture capital has become glorified, and too often, we see founders chasing VC with businesses that don’t fit the venture model. There is nothing wrong with building a business that isn’t a fit for venture and it doesn’t make it any less of a worthwhile pursuit. It just means it needs to be financed differently. Remember, raising venture capital is a treadmill that only gets faster and steeper over time (VC Minute episode 16).

🐸 Leapfrogging

Rock Health published a Q1 2025 healthtech market overview in which they discuss the high-level state of venture in healthtech and how companies are navigating a particularly uncertain time across the industry. Similar to the above article, the focus might be on healthtech, but the takeaways are generalizable. The below image is a good summary of the four ways Rock Health sees companies succeeding in the current environment.

STV Take: The two questions that kept running through my mind as I read this are the following 1) How does the Hinge Health IPO (fingers crossed 🤞) impact the healthtech environment, especially at the later stage? 2) As seed companies run out of runway without the revenue or revenue growth to raise a subsequent round, will M&A (honestly, probably acquihires and fire sales) heat up? Will that make the acquiring businesses more durable? How does that impact early-stage investor sentiment?

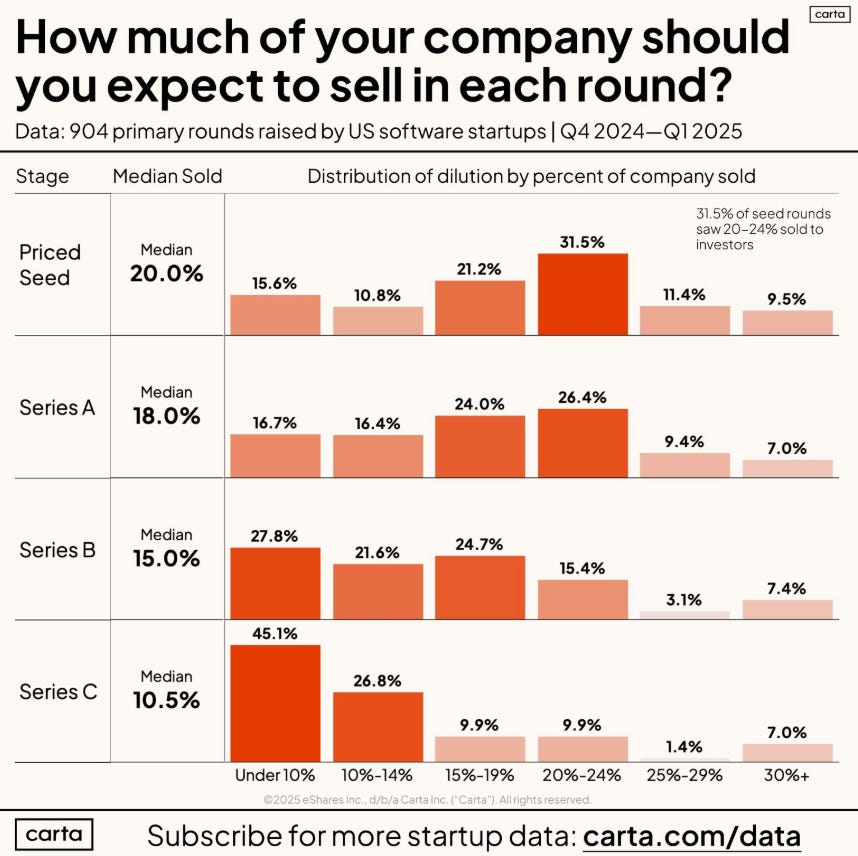

📌 How Much Equity Should Founders Give Up?

Peter Walker shared a LinkedIn post detailing the amount of equity founders give up at each round, based on Carta data. Unsurprisingly, less than 10% of software Seed rounds had founders selling more than 30% of the business. For Seed rounds, the median amount sold is 20%, and at the Series A it is 18%.

STV Take: Transparency around the typical amount founders sell at each stage helps both founders and investors have realistic expectations around ownership. Raising venture capital is hard. Don’t make raising future rounds harder by straying too far from the market norm, even if it means holding off on fundraising until there are more proof points around the business that enable you to have more bargaining power in fundraising conversations.

Well said or stated.

The gap between Venture bankable and otherwise is less obvious now, but substantially wider as companies evolve